Should I Stay or Should I Go?

29 March 2020

Not the time for panic selling

With most major stock markets down around 30 – 35% at the time of writing, many investors are probably left wondering whether they should stay in the markets or go to cash or something less risky.

Prior to the COVID-19 outbreak, markets were experiencing one of the longest bull markets in history, now many investors are left wondering where to next as we face an unprecedented moment in recent history.

The emotions we feel when markets are behaving like they are at the moment are completely normal and you can be forgiven for thinking investment markets are not for you or that you will be happy just having your money in the bank.

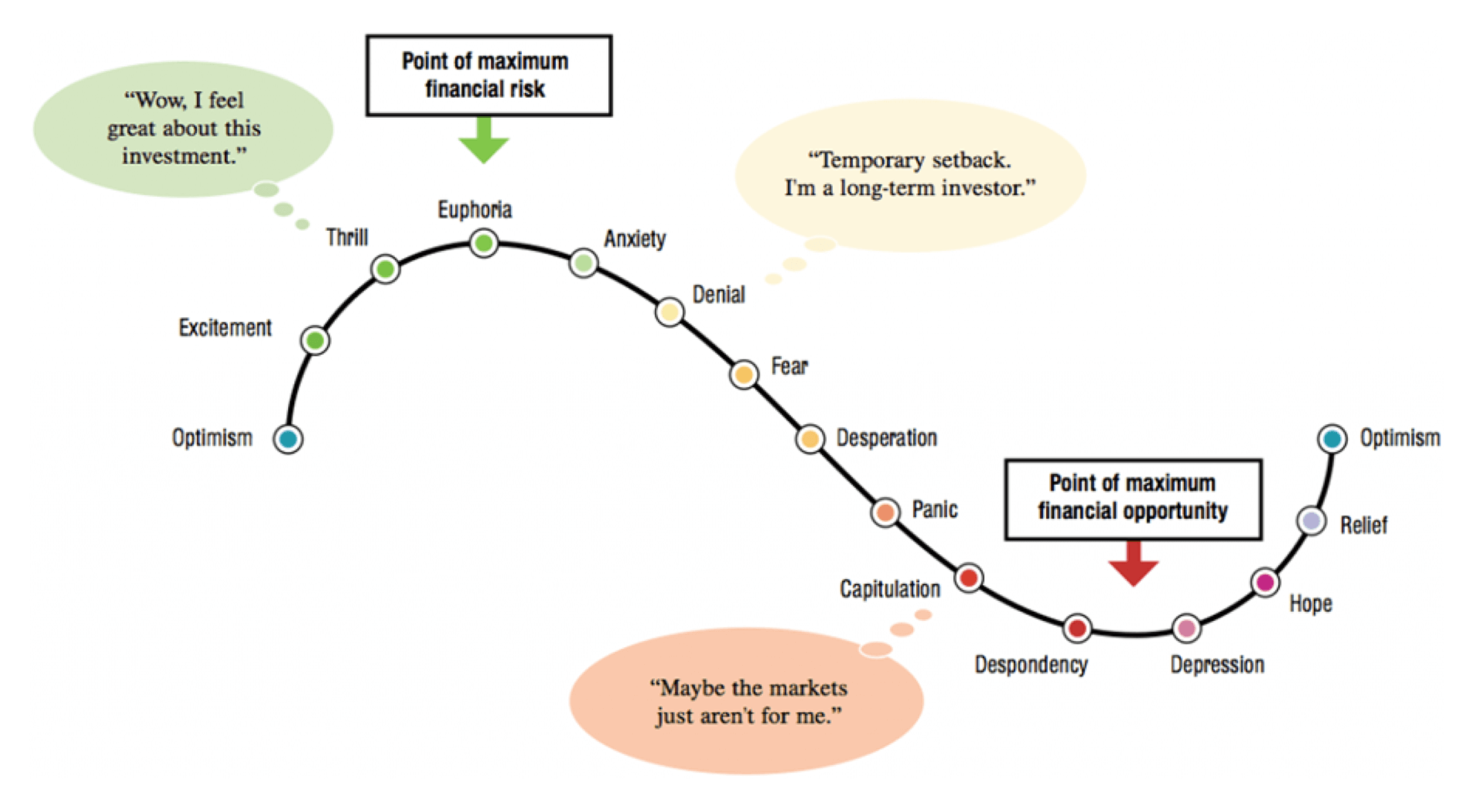

The cycle of market emotions graph below has been around for decades and through many market cycles. It simply explains how we are all feeling at different times of the market cycle, both when things are going well and when things are not, as we find ourselves in this period.

As you can see below, when we are feeling the emotion, “Capitulation” (selling and going to cash), this is nearing the bottom of the cycle and in many ways the wrong time to sell, as it is the “point of maximum financial opportunity”.

I will also point you to the top of the cycle, this is where we have all been over the past few years, a time when we have felt “Euphoria”

feeling how good the share market is, and how happy we feel about our investments, yet this was the time when we were at the maximum risk.

At InvestSense we are very aware of the market cycles and consequently, the portfolios have been well-diversified, also in most cases, we had less of your money exposed to expensive shares than many other investment portfolios in the market.

We also have allocations to cash and other non-share investments in the portfolio which we will look to deploy into the portfolio as we get closer to the bottom of the cycle “point of maximum financial opportunity”.

Generally, after share markets have had a large selloff, they tend to rebound quite strongly, this is why selling out of shares and moving into cash near the bottom of the cycle can be the worst action to take, especially when money in the bank is not even keeping up with inflation, in reality, the value of your money is going backwards.

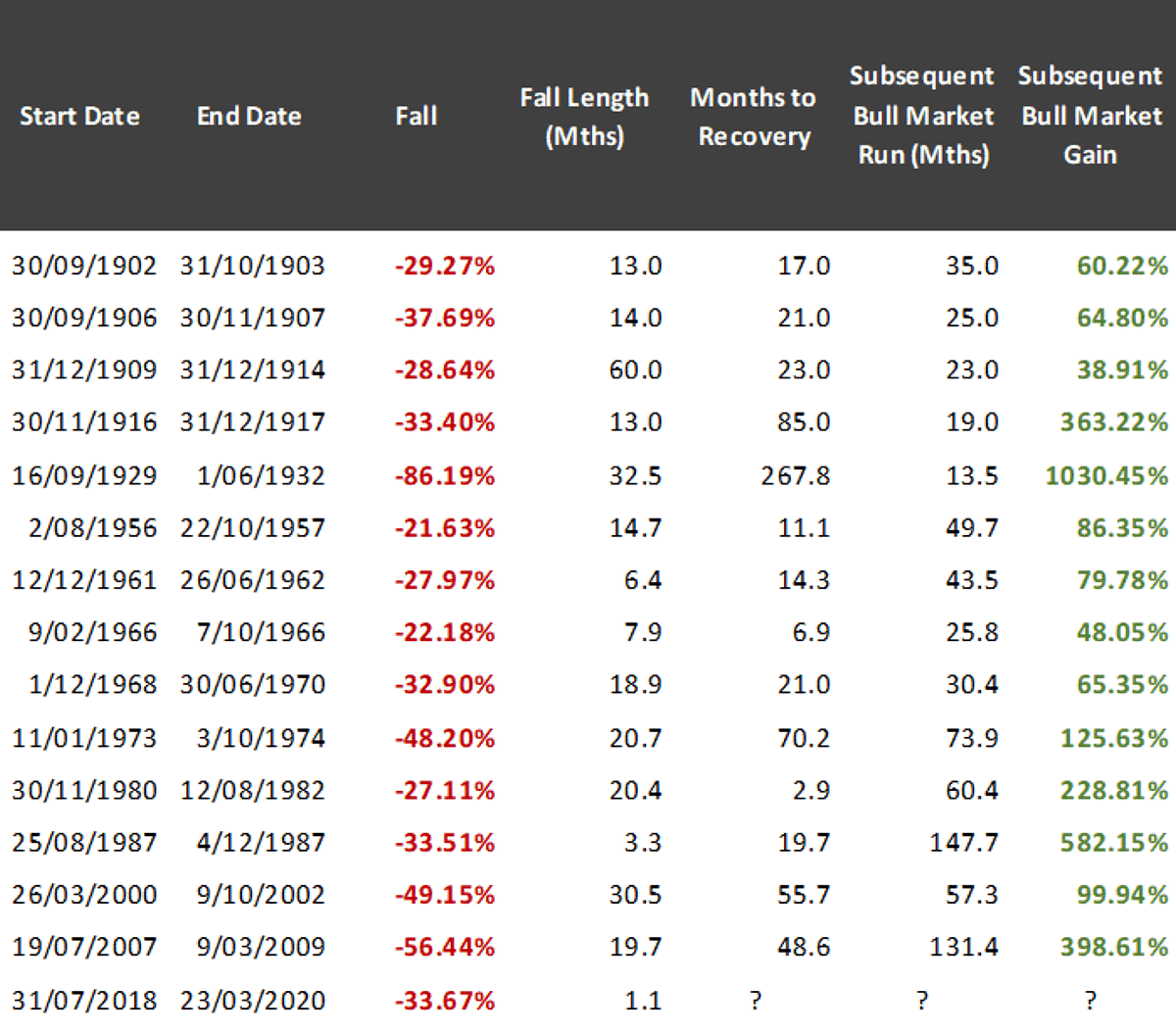

To help provide some context around how recoveries have played out historically, the chart below outlines some of the larger market falls that US equities experienced over the last 120 years and then how they have recovered. It can take some time to recover and this is where you will need to be patient.

To find out more about setting up a Mulcahy & Co Investment Account, please download the document below:

Latest News

The government has announced it will make some practical changes to its proposed tax changes for people with large super balances (over $3 million) that will now take effect from 1 July 2026.

Big changes are on the way for aged care, with new rules starting from 1 November 2025. While these changes aim to create a more sustainable and fairer system, they do bring added complexity — especially when it comes to understanding the fees and making the right financial decisions. Here are the five key things you need to know: 1. Aged care will cost more - but is still subsidised If you or a loved one is moving into residential aged care from 1 November 2025, the amount you’ll need to contribute will be higher. That said, the Government will continue to fund a large share of care costs - around 73% on average. But it will be important to consider your cashflow. 2. Expect new terminology and fee calculations The language is changing. Instead of the current “means-tested care fee,” you’ll now see new names like Hotelling Contribution and Non-Clinical Care Contribution. How much you are asked to pay will still be based on your income and assets, but new formulae may result in higher contributions than under the current rules. 3. Lifetime caps remain – but at a higher level A lifetime cap will continue to apply to limit how much you can be asked to pay as a non-clinical care contribution over your total stay in residential care. This cap is increasing to $130,000, but with a new safeguard, that no matter how much you pay, you will only need to pay this fee for a maximum of four years. This helps ensure fairness between residents with different levels of wealth. 4. Retention amounts are being reintroduced If you choose to pay a lump sum for your room (known as a refundable accommodation deposit - RAD), aged care providers will deduct a “retention amount” of up to 2% per year (capped at 10% over five years). While this increases the cost slightly, it may still be better value than paying the daily accommodation payment. 5. Good advice can prevent costly mistakes Navigating these new rules can be confusing - especially when you need to make major decisions about the family home, assets or pension entitlements. The cost of getting good advice is often small compared to the cost of getting it wrong. That’s why seeking qualified aged care financial advice is more important than ever. If you're starting to think about aged care for yourself or a family member, now is the time to start planning and seek advice. As specialists in aged care advice, we can help you to make informed decisions with confidence and peace of mind. Please contact Lynde via the link below to chat more about these changes.

Victoria's 'Commercial and Industrial Property Tax Reform' and how this will affect Stamp Duty for these properties is discussed with Principal Solicitor Brad Matthews and host Gavin Nash. Changes are coming on July 1st 2024 in this area and Brad gives us great insight into how and what is changing - and when!

Victoria's 'Vacant Residential Property Tax' is discussed with Principal Solicitor Brad Matthews and host Gavin Nash. Changes are coming on July 1st 2024 in this area and Brad gives us great insight into how and what is changing - and when!